This article is for informational purposes only and does not constitute legal, financial, or real estate advice please consult a attorney.

Are you falling behind on your mortgage payments in Ohio? You’re not alone in facing the possibility of a writ of possession. Thousands of Ohio homeowners face this challenge every year, but effective Ohio mortgage foreclosure prevention strategies can help you avoid losing your home and protect your financial future. This comprehensive guide outlines seven proven approaches you can implement today to address mortgage default and keep a roof over your head.

Important: The sooner you act, the more options you’ll have available. Don’t wait until it’s too late.

Need immediate help with your mortgage situation? EasySell Cash Homebuyers in Columbus can provide a fast, stress-free solution. Call us today at (614) 969-0624 for a free, no-obligation cash offer on your home.

Ohio mortgage foreclosure prevention: Understanding Ohio’s Foreclosure Timeline & Process

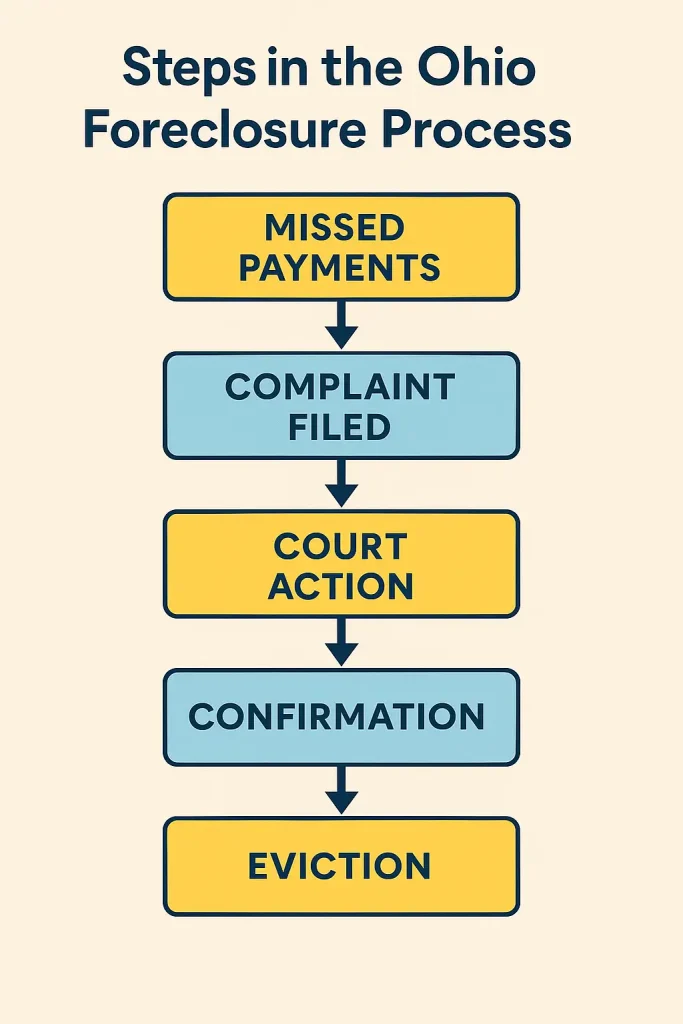

Ohio follows a judicial foreclosure process, making it different from many other states. Understanding this timeline can help you strategically plan your mortgage foreclosure prevention efforts.

Pre-Foreclosure Notice Period in Ohio

When you miss payments in Ohio, your lender typically follows this process:

- 30 days late: Your lender will contact you about the missed payment

- 45-60 days late: You’ll receive a formal “breach letter” stating you’ve violated the loan terms

- 90-120 days late: The lender may file a foreclosure lawsuit

During this pre-foreclosure period, you have the most options available to resolve the situation.

Judicial Foreclosure Process Timeline

Ohio’s judicial foreclosure process typically includes:

- Complaint filing: The lender files a foreclosure lawsuit in your county court

- Service of process: You receive official notice of the lawsuit (summons and complaint)

- Response period: You have 28 days to respond to the complaint

- Court proceedings: If contested, the case moves to hearings and potentially trial

- Judgment: If the court rules for the lender, a judgment of foreclosure is issued

- Sale scheduling: The property is scheduled for sheriff’s sale (typically 30-60 days after judgment)

- Sheriff’s sale: Property is auctioned to the highest bidder

- Confirmation of sale: Court confirms the sale (typically within 30 days)

The entire Ohio foreclosure timeline from missed payment to sale typically takes 6-12 months, depending on court backlogs and whether you contest the foreclosure.

Post-Judgment Rights in Ohio

Even after a foreclosure judgment, Ohio property owners retain important rights:

- Right of redemption: You can “redeem” your property by paying the full judgment amount before the confirmation of sale

- Deficiency judgment protection: In some cases, you may have defenses against deficiency judgments

7 Effective Ohio Mortgage Foreclosure Prevention Strategies

If you’re struggling with mortgage payments, implementing these seven proven foreclosure prevention strategies can help save your Ohio home:

1. Contact Your Lender (Script Template Included)

Opening communication with your lender is crucial. Many people avoid this conversation out of embarrassment or fear, but lenders often prefer working with you over foreclosure.

Sample script when calling your lender:

“Hello, my name is [Your Name], and my loan number is [Loan Number]. I’m experiencing financial hardship due to [brief explanation]. I want to keep my home and continue making payments. What loss mitigation options are available to me?”

2. Document Your Financial Hardship

Create a file documenting your financial situation to support your case against summary judgment.

- Income reduction or job loss verification

- Medical bills or disability documentation may be relevant when you file an answer to the foreclosure complaint.

- Divorce decree or separation agreement

- Death certificate (if applicable)

- Other relevant hardship evidence

This documentation will be essential when applying for assistance programs or negotiating with your lender.

3. Apply for Ohio Homeowner Assistance Fund

The Ohio Homeowner Assistance Fund (OHAF) provides financial help to eligible applicants who are behind on their mortgage payments due to pandemic-related hardships. This program can provide up to $35,000 in assistance to qualified applicants.

To be eligible, you must:

- Own and occupy the property as your primary residence

- Have experienced a qualified financial hardship after January 21, 2020

- Have income at or below 150% of the area median income

Apply through the official OHAF website or call 888-362-6432 for assistance.

4. Consider Loss Mitigation Options for Ohio Mortgage Foreclosure Prevention

Your lender may offer several loss mitigation options to prevent foreclosure:

- Forbearance: Temporarily reduces or suspends mortgage payments

- Repayment plan: Spreads missed payments over a specific timeframe

- Loan modification: Changes loan terms to make payments more affordable

- Partial claim: Defers missed payments until the end of the loan (FHA loans)

Contact your loan servicer to request a loss mitigation application.

5. Understand Your Legal Rights

Ohio foreclosure laws provide specific protections for homeowners. Knowing your rights can help you navigate the process more effectively:

- You have the right to reinstate your loan before judgment

- You have redemption rights until the confirmation of the sheriff’s sale

- You can request mediation in many Ohio counties

- Your lender must provide proper notice before foreclosure, as required by ohio law.

6. Explore Bankruptcy Protection

Chapter 13 bankruptcy can:

- Stop foreclosure proceedings immediately

- Allow you to catch up on missed payments over 3-5 years

- Potentially eliminate second mortgages in some cases

- Provide court protection while you reorganize your finances

Consult with a bankruptcy attorney to determine if this option is right for your situation before you file a motion.

7. Consider Selling Your Home

If keeping your home isn’t feasible, selling before foreclosure can protect your credit and potentially provide funds for a fresh start. Options include traditional sales, short sales, or selling to a cash buyer like EasySell Cash Homebuyers.

Ohio-Specific Mortgage Assistance Programs (2025)

Several assistance programs are available specifically for Ohio homeowners facing foreclosure, including those who may need to file a motion.

Ohio Homeowner Assistance Fund (OHAF) Eligibility

As mentioned above, OHAF provides crucial assistance to qualifying homeowners. The program can help with preventing foreclosure and obtaining a summary of your financial situation.

- Delinquent mortgage payments

- Property taxes

- Homeowner’s insurance

- HOA fees

- Utilities

The maximum assistance amount is $35,000 per household. Funds are distributed directly to your mortgage servicer or other entities.

HUD-Approved Counseling Services in Ohio

HUD-approved housing counselors provide free or low-cost guidance to help you understand your options:

- Budget counseling

- Mortgage delinquency counseling

- Foreclosure prevention strategies

- Assistance with lender negotiations

Find a HUD-approved counselor in Ohio by calling 800-569-4287 or visiting the sheriff’s office for assistance. HUD counselor finder.

County-Level Assistance Programs

Many Ohio counties offer additional assistance programs:

- Cuyahoga County: Foreclosure Prevention Program

- Franklin County: Emergency Mortgage Assistance Program

- Hamilton County: Home Improvement Program

- Montgomery County: Homeownership Center

Contact your county treasurer’s office or housing department for information about local programs.

Ohio Legal Aid Resources for Homeowners

Free or low-cost legal assistance is available through:

- Ohio Legal Aid

- Legal Aid Society of Columbus

- Legal Aid Society of Cleveland

- Pro Seniors (for people 60+)

These organizations can help you understand the foreclosure process, review your case, and potentially represent you in court.

Alternatives to Foreclosure for Ohio Homeowners

If keeping your home isn’t feasible, several alternatives can help you avoid foreclosure:

Loan Modification vs. Refinancing Options

Loan Modification:

- Changes your existing loan terms

- May reduce interest rate or extend loan term

- Doesn’t require good credit

- No closing costs

Refinancing:

- Replaces your current loan with a new one

- Requires good credit and home equity

- Includes closing costs

- May provide lower interest rates

Your best option depends on your credit score, equity position, and financial situation.

Short Sale Process in Ohio

A short sale allows you to sell your home for less than you owe on the mortgage, with your lender’s approval. Benefits include:

- Less damage to your credit than foreclosure

- Potential for relocation assistance

- Possibility of debt forgiveness

- Control over the sale process

To pursue a short sale, contact your lender’s loss mitigation department for their specific requirements and procedures.

Deed in Lieu of Foreclosure

With a deed in lieu, you voluntarily transfer ownership of your property to the lender in exchange for release from your mortgage obligation. This option may help you file an answer to the foreclosure complaint.

- Is faster than foreclosure

- May include relocation assistance

- Has less negative credit impact than foreclosure

- Provides a clean break from the property

Not all lenders offer this option, and you typically must attempt to sell the property first.

Chapter 13 Bankruptcy Protection

Chapter 13 bankruptcy can:

- Stop foreclosure proceedings immediately

- Allow you to catch up on missed payments over 3-5 years

- Potentially eliminate second mortgages in some cases

- Provide court protection while you reorganize your finances

Consult with a bankruptcy attorney to determine if this option is right for your situation.

Selling Your Ohio Home to Prevent Foreclosure

Selling your home can be a viable solution to avoid foreclosure and protect your credit.

Traditional Sale vs. Quick Cash Offer

Traditional Sale:

- Often brings higher sale price

- Takes longer (typically 60-90 days)

- May require repairs and improvements

- Involves negotiation, inspections, and contingencies that could prevent summary judgment.

Cash Sale to Investor:

- Faster closing (sometimes as quick as 7-14 days)

- No repairs needed (sold “as-is”)

- No commissions or closing costs

- Generally lower sale price

Local Solution: As a locally-owned business in Columbus, EasySell Cash Homebuyers can purchase your home in any condition, often closing in as little as 7 days. We handle all paperwork and closing costs, allowing you to walk away with cash and avoid foreclosure. Call (614) 969-0624 to get your no-obligation cash offer today.

For a detailed guide on selling quickly in Columbus, check out our article on how to sell my house fast in Columbus Ohio.

How to Sell While in Pre-Foreclosure

Selling during pre-foreclosure requires careful timing:

- Determine your payoff amount from your lender

- Get a realistic market value assessment

- Decide between traditional sale or cash investor

- List the property or contact investors

- Review offers with your payoff amount in mind

- Coordinate closing with your lender

For more information on selling your house as-is, read our complete guide to selling your house as-is in Columbus Ohio.

Using Home Equity to Resolve Debt

If you have significant equity, selling may allow you to avoid the writ of possession.

- Pay off the mortgage completely

- Cover any tax liens or judgments

- Potentially walk away with cash for a fresh start

- Avoid damage to your credit from foreclosure

Avoiding Foreclosure Rescue Scams in Ohio

Unfortunately, owners in distress often become targets for scams. Protect yourself by recognizing the warning signs.

Red Flags to Watch For

Be wary of anyone who:

- Guarantees to stop foreclosure

- Tells you not to contact your lender

- Asks for upfront fees

- Tells you to make payments to them instead of your lender

- Pressures you to sign documents you don’t understand

Legitimate vs. Predatory Investors

Legitimate Investors:

- Provide clear, written offers

- Encourage you to seek legal advice

- Have verifiable references and reviews

- Allow time for consideration

- Can provide proof of funds

Predatory Investors:

- Create urgency and pressure

- Offer verbal-only agreements

- Have complex, confusing contracts

- Target vulnerable property owners

- Use high-pressure sales tactics

For more information on spotting scams, read our article on we buy houses in Columbus cash offer scam.

How to Report Fraud in Ohio

If you believe you’ve encountered a foreclosure rescue scam:

- Contact the Ohio Attorney General’s Office: 800-282-0515

- File a complaint with the Consumer Financial Protection Bureau

- Report to your local Better Business Bureau

- Notify your county prosecutor’s office

Success Stories: Ohio Homeowners Who Avoided Foreclosure

Case Study: Loan Modification Success

John and Maria from Cincinnati were four months behind on their mortgage after John lost his job. By working with a HUD-approved counselor, they secured a loan modification that reduced their interest rate from 5.5% to 3.2% and extended their term. This lowered their monthly payment by $450, making it affordable on Maria’s income until John found new employment.

Case Study: Assistance Program Beneficiary

Darlene, a senior in Cleveland, fell behind on payments after unexpected medical bills. Through Ohio’s Homeowner Assistance Fund, she received $18,000 to bring her mortgage current and an additional three months of payment assistance while she recovered. Today, she’s back on track with her payments and no longer facing foreclosure.

Frequently Asked Questions

How long does the foreclosure process take in Ohio? The typical judicial foreclosure process in Ohio takes 6-12 months from the first missed payment to auction, depending on court backlogs and whether the homeowner contests the foreclosure.

Can I still save my home after receiving a foreclosure notice in Ohio? Yes, even after receiving a foreclosure notice, Ohio homeowners have several options including loan modification, repayment plans, or applying for assistance through the Ohio Homeowner Assistance Fund (OHAF). You maintain redemption rights until the final sale.

Will I still owe money after foreclosure in Ohio? Possibly. Ohio allows lenders to pursue a deficiency judgment if the foreclosure sale doesn’t cover the loan balance. However, you may have defenses against these judgments, especially if you pursue alternatives like short sales with deficiency waivers.

How will foreclosure affect my credit score? A foreclosure can reduce your credit score by 100-250 points and remain on your credit report for seven years. However, alternatives like loan modifications or short sales typically have less severe impacts.

Can I sell my house during foreclosure in Ohio under ohio law? Yes, you can sell your property until it’s sold at sheriff’s sale. For insights on selling to investors, read our guide on pros and cons of selling to a real estate investor in Columbus Ohio.

Final Thoughts: Ohio Mortgage Foreclosure Prevention Is Possible

Falling behind on mortgage payments is stressful, but numerous resources and options are available to help Ohio homeowners. The key is taking action early and understanding all your alternatives for foreclosure prevention.

Whether you choose to work with your lender on a loan modification, apply for assistance programs, sell your home, or explore legal options, remember that you don’t have to face this challenge alone.

For homeowners considering working with real estate investors or wholesalers, be sure to read our article on real estate wholesalers in Columbus Ohio to understand how these arrangements work.

Get Help From Columbus’s Ohio Trusted Home Buyers

At EasySell Cash Homebuyers, we understand the stress and uncertainty that comes with mortgage default. As a locally-owned Columbus business, we’ve helped Ohio homeowners avoid foreclosure through our fast, fair cash purchase program.

How we can help:

- Get a cash offer within 24 hours to avoid the foreclosure complaint process.

- Close in as little as 10 days (or on your timeline)

- No repairs, cleaning, or showings required

- No fees or commissions

- Flexible moving timeline

- Professional guidance through the entire process

Need personalized assistance? Call EasySell Cash Homebuyers today at (614) 969-0624 for a free, no-obligation consultation about your specific situation.

This article is for informational purposes only and does not constitute legal, financial, or real estate advice. Foreclosure laws and timelines can vary by county and individual circumstances. Homeowners facing foreclosure in Ohio should consult with a licensed attorney, financial advisor, or HUD-approved housing counselor to discuss their specific situation.